In recent months, the investment community observed the passing of Charlie Munger and Daniel Kahneman. Munger and Kahneman came from different disciplines but shared the same objective: improving judgment in an uncertain world blurred by bounded rationality. Both searched for signal from noise, which is the essence of investing.

Venture capital and private equity seek alpha, or superior investment performance, by looking for signal from noise. Pattern recognition derives signal from noise yielding investment insight but may also color one lens and blind investors to new opportunities or market shifts. Seeking alpha is thus a two-edged sword that must be wielded prudently.

Kahneman and Munger identified several biases that impede good judgment in noisy, uncertain conditions. This article summarizes these biases and provides a framework for how an investor can improve investment performance by reducing bias and noise. In my next article on Superforecasting, I discuss ten investment practices to improve decision making and investment performance based on work Kahneman, Tetlock and Munger as well as investment practices we have used at NGP Capital and observed applied effectively at other venture firms.

Seeking Wisdom: Kahneman and Munger

Nobel laureate Daniel Kahneman founded behavioral economics upending rational expectations, a microeconomic theory that assumes people make predictably rational decisions with full information. Instead, Kahneman believed we live in an uncertain world with partial information in which judgments err predictably. In his initial study, Judgment under Uncertainty: Heuristics and Biases written in 1974, Kahneman posited three propositions: (1) people are not generally aware of the rules that govern their impressions; (2) people cannot deliberately control their perceptions; but (3) they can learn to recognize situations in which impressions are likely to be biased and deliberately make appropriate corrections.[1] His recent books Thinking, Fast and Slow and Noise: A Flaw in Human Judgment summarize his research over the past five decades, which reinforces his early insights.

Charlie Munger, a private equity investor and partner with Warren Buffett, echoed Kahneman: “If you want to avoid irrationality, it helps to understand the quirks in your own mental wiring and then you can take appropriate precautions.”[2] Munger developed a checklist of one hundred mental models that he used to evaluate each investment. A third of his checklist involved tendencies or biases that lead investors astray. Having delivered superior returns for more than five decades, Berkshire Hathaway has garnered a wide following, especially with their annual letter to shareholders and investor gathering. If Buffett is the Oracle from Omaha, then Munger was its prophet. Munger wrote little but, as Aristotle did for Socrates, others have written books sharing wisdom from his few public speeches. Notable books include Poor Charlie’s Almanack by Peter Kaufman and Seeking Wisdom by Peter Bevelin.

The Prudent Man Principle: Good Judgment Essential for Investing

Efforts to improve judgment involve significant cognitive and organizational costs. As a result, Daniel Kahneman forewarned that these costly efforts may not be appropriate in all cases. We may rely on instinct for most routine decisions — what Kahneman describes as ‘thinking fast’. ‘Thinking slow’ is reserved for consequential, non-routine decisions.[3] Jeff Bezos, founder of Amazon, applied similar logic in his distinction between one-way and two-way doors[4]. Two-way doors are reversible decisions that may be made quickly. One-way doors are irreversible decisions that require greater care, especially when they involve significant resource commitments.

Venture capital and private equity investments are one-way doors and ‘thinking slow’ exercises. Unlike buying stock in public securities, investments in private companies are illiquid and not readily reversible. Venture firms make only a few investment decisions annually upon which their reputation depends. Warren Buffett advised people to invest carefully as though they have only ten investments to make in their life. For the average young investment professional, Buffett’s guidance is not a thought experiment but a reality.

The prudent man principle stipulates that institutional investors have a fiduciary responsibility to invest assets as a “prudent man” would with his own property. Fiduciaries entrusted to invest another’s assets is a significant undertaking that deserves the utmost care and diligence. Yet prudence is tested in hot, highly competitive markets that conspire to lower investment standards. Buffett observed, “What the wise do in the beginning, fools do in the end.”[5] Charlie Munger acknowledged, “I came to the psychology of human misjudgment almost against my will; I rejected it until I realized that my attitude was costing me a lot of money.”[6] Buffett and Munger lived far from investment centers to avoid market groupthink and sought to keep their heads when markets lost theirs.

Few industries value good judgment as highly as the investment profession. Investment judgment is a prerequisite for survival and highly rewarded when positively demonstrated. Investors must deliver market rates of return to maintain investor confidence. Consistently delivering superior returns confers more market influence and assets under management.

Errors in Judgment: Bias and Noise

Good investment judgment involves making accurate, insightful investments that seem prescient in hindsight. Yet, in an uncertain world, there are many sources of variance that loosen the relationship between decisions and outcomes. Markets fluctuate in ways few investors can anticipate. Passive investors have little or no influence on company performance. Thus, good outcomes can come from bad decisions and bad outcomes can come from good decisions. As former head of Goldman Sachs Robert Rubin reminds us, “Decisions shouldn’t be evaluated only based on results. Even the best decisions are probabilistic and run a real risk of failure, but the failure wouldn’t necessarily make the decision wrong.”[7]

As Nassim Taleb observed based on his trading experience, it is easy to be Fooled by Randomness: it is rarely clear whether investors are good because they are lucky or lucky because they are good. Instead, investors should focus on making consistently good decisions and trust good outcomes will follow across a portfolio of investments.

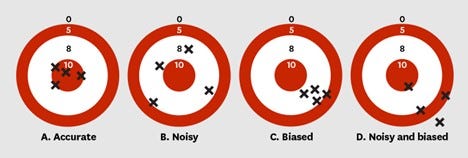

Munger was assiduous and systematic in his efforts to make consistently good investment decisions. Munger’s efforts led him to Kahneman, who saw noise as a source of variability and bias as a distortion of accurate judgment. Kahneman illustrated the consequences of poor judgment introduced by bias and noise with the following graphic:

Figure 1: Errors in Judgment — Bias and Noise[8]

Investors maximize expected returns by making consistently accurate investment decisions as shown in target A. Yet unconscious biases distort judgment in predictable ways. Some tendencies produce more variability in the decision-making process, which Kahneman describes as noisy decisions as shown in target B, while biases yield predictable errors as shown in target C. When decisions are both noisy and biased, we see results that are both scattered and off kilter as shown in target D.

Predictably Irrational: Reducing Bias and Noise

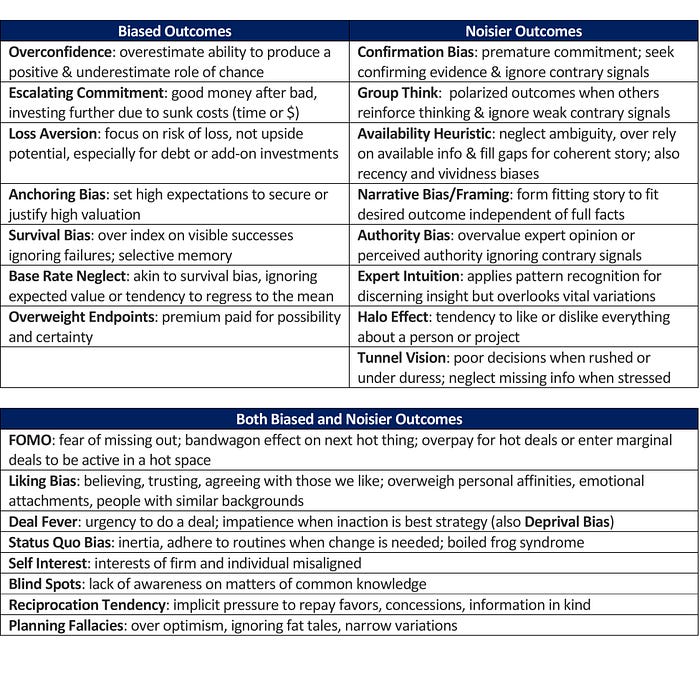

Humans are predictably irrational.[9] While over 180 cognitive biases have been identified, Kahneman focused on twelve in Noise, his latest book, and Charlie Munger included those twelve plus others among the 25 he highlighted in his various speeches.[10] In Figure 2, I have summarized these tendencies and placed them into three categories consistent with Kahneman’s distinction between signal and noise in Figure 1. The first column describes biases that lead to consistent errors of judgment and skew assessments akin to target C in Figure 1. The second column summarizes tendencies that increase noise adding variability to investment outcomes like target B in Figure 1. The third category at the bottom show heuristics that may yield both biased and noisier decisions depending on the context.

Figure 2: How Cognitive Tendencies Produce Biased and Noisier Outcomes

Munger observed that biases tend to cluster, which can contribute to calamitous outcomes he called lalapaloozas: “When you get two or three of these psychological principles operating together, then you really get irrationality on a tremendous scale.” At NGP Capital, our investment experience corroborates this. In our portfolio review of investments made over fifteen years, we found that investments decisions that produced losses had three times more biases than those with outcomes that yielded a 3x or more return. While there is surely some Monday morning quarterbacking in this assessment, our internal review provides ample evidence that bias and noise negatively impacts investment performance.

Investor Returns: Seeking Alpha While Reducing Beta

Investors seek alpha while minimizing beta, two measures of superior investment performance. As both Berkshire Hathaway and NGP Capital have observed, good judgment is involved in both.

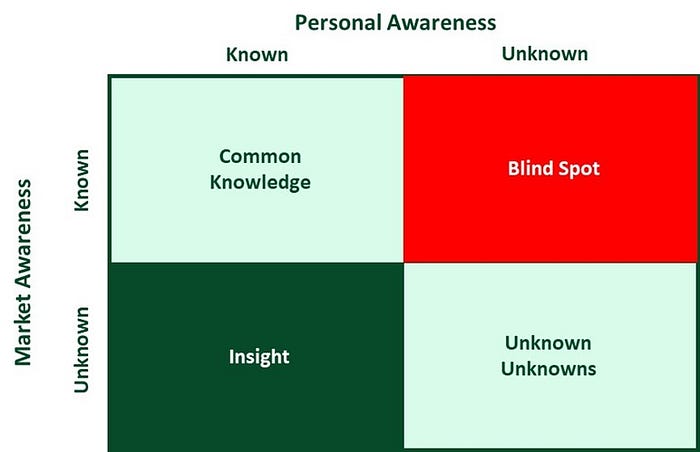

Alpha measures the returns premium reliably realized relative to a relevant benchmark index. Alpha derives from insights that yield consistently superior investments. Generating alpha is rare in highly competitive markets. Common knowledge is not a source of alpha but could be a potential blind spot if overlooked by an investor. Windfalls resulting from serendipitous events — what lawyers describe as ‘acts of god’ and Rumsfeld called unknown unknowns — are not reliably repeatable and thus not sources of alpha. In seeking alpha, investors look to develop expertise while reducing blind spots as shown in Figure 3.

Figure 3: Seeking Alpha — Developing Insight while Reducing Blind Spots

Investment returns include a second component ‘beta’, which measures rate of return variability. Investors think of beta as risk. Riskier investments demand higher returns, so an investor could increase expected return by assuming higher risk. Prior returns are useful indicators of future performance only if they are repeatable. Investment returns with lower beta are less risky and more repeatable.

Beta is a natural artifact of market fluctuations and changes in company performance. Early-stage investing is inherently noisy. As Tom Alberg, founder of Madrona Ventures observed, “Even with rigorous due diligence, most early-stage investments come down to an informed hunch.”[11]

A stochastic environment makes it even more important to establish a few fixed reference points. A thoughtful investment strategy and systematic process provides common guideposts for investors and reinforces consistency in volatile, cyclical markets. A systematic investment process improved investment performance by reducing noise, or beta, while improving alpha.

My next blog describes ten investment strategies and processes to reduce bias and noise helping to improve investment performance.

Footnotes:

[1] Tversky, A., Kahneman, D. (1974). Judgment under Uncertainty: Heuristics and Biases. Science.

[2] Bevelin, P. (2018). Seeking Wisdom — From Darwin to Munger, third edition. PCA Publications LLC.

[3] Kahneman, D. (2011). Thinking, Fast and Slow. Macmillan.

[4] Jeff Bezos explained decision making based on one-way and two-way doors in Amazon’s 2016 annual letter to shareholders.

[5] Warren Buffett at the 2006 Berkshire Hathaway Annual Meeting.

[6] Bevelin(2018). Seeking Wisdom.

[7] Robert Rubin, In an Uncertain World.

[8] Kahneman, D., Rosenfield, A.M., Gandhi, L. & Blaser, T., (2016). Noise: How to Overcome the High, Hidden Cost of Inconsistent Decision Making. Harvard Business Review, October 2016.

[9] Ariely, D., & Jones, S. (2008). Predictably irrational (p. 20). New York: HarperCollins.

[10] Kaufman, P.D. (2023). Poor Richard’s Almanac. PCA Publications. Bevelin (2008) identified 28 relevant to investments in his broader review of Munger and others.

[11] Alberg (2021). Flywheels.