The Five Forces: Five Startup Strategies for Winner Take Most Markets

“Full many a flower was meant to blush unseen and waste its fragrance on the desert air. Full many a man was meant to scale the heights but faint of heart turned back when almost there.” Sir Thomas Moore, Elegy in a Country Churchyard

Does the person make the time or time make the person? One of the great debates of history, this question also applies to entrepreneurs. Do investors bet on the team or market?

Early-stage investors bet on the team. An A team can sometimes make a B plan work, but an B team will screw up an A plan every time. Two added considerations shift chips toward the founding team: (1) Founder Fit precedes Product Market Fit; and (2) good teams can pivot in search of Product Market Fit.

In private equity, the situation is reversed: markets have primacy over teams. As control investors, private equity can backfill management with trusted executives. Firms and markets are well established, so private equity has more at stake in getting the market right.

History suggests these questions pose a false choice: a person may make the time but only if timing is opportune. But for the advent of World War II, British Parliament would not have elected Winston Churchill as Prime Minister and U.S. Generals Marshall and Eisenhower would have retired anonymously. But for the COVID pandemic, Dr. Fauci could have lived a quiet life. But for the attack by Russia, Zelenskyy would be unknown outside of Ukraine.

Entrepreneurs author startup success, yet markets circumscribe the opportunity horizon. Vinod Khosla observed after decades of investing that “entrepreneurs only control 30–40% of the factors that affect their success. Competitors and environmental circumstances make up the rest.” Warren Buffett similarly quipped, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

For investors, fortune favors the prepared mind. As discussed in the Three Cardinal Sins of Investing, investors win when the right team converges on the right market. Why then do Board discussions ignore market activity?

Entrepreneurs and investors should measure twice on markets before cutting once. Markets have a gravitational pull that, like black holes, is hard to escape once within their boundaries. Entrepreneurs devote years, sometimes careers, in an industry. Investors tend to specialize so are wise to start fishing in well stocked ponds rather than dry holes. While flowers may blush unseen and waste their fragrance on the desert air, talent and capital are far too valuable to be similarly misspent.

Industry Structure: The Five Forces Framework

Michael Porter is a clarion voice for the primacy of markets. In his business classics Competitive Strategy and Competitive Advantage, market structure is the gravitational force that dictates competitive dynamics and firm profitability. Markets evolve but industry structure remains stable and is discernible in advance, so entrepreneurs and investors should understand well the markets they intend to enter.

The Five Forces Model has been the leading framework to assess industry structure since Porter introduced it in 1980. The Five Forces Model suggests that, while markets fluctuate, competitive dynamics evolve predictably across an industry lifecycle consistent with the underlying industry structure.

Figure 1: The Five Forces Model

The Five Forces Model identifies key factors that influence competitive dynamics and ultimately premeditate industry structure. Firms compete for profits with suppliers and customers as well as competitors. With this broader perspective, five forces determine industry profitability and influence how profits are shared among participants: (1) rivalry among existing competitors; bargaining power of (2) suppliers and (3) customers; and threats posed by (4) potential competitors and (5) substitute products. Following is a summary of how these forces influence competitive dynamics and industry structure:

· Competitive rivalry evolves over the industry lifecycle as illustrated in Figure 2. At the outset, competition is benign as firms share costs to establish customer awareness, market validation and Product Market Fit, especially when Crossing the Chasm from early adopters to mainstream customers. Competition escalates yet remains moderate during the high growth phase as firms focus on scaling their business and fulfilling increasing demand. Slower growth, however, heightens competitive rivalry and accelerates industry consolidation. As markets mature, industry structure ultimately depends on product differentiation, capital intensity, economies of scale and barriers to entry. Competitive rivalry, industry concentration, brand loyalty and switching costs derive from industry structure.

Figure 2: Changing Competitive Dynamics Across Industry Lifecycle

· Supplier and customer relationships are complex. Companies coordinate supply chains with suppliers and serve customer needs, yet negotiations with suppliers and customers determine how profits are shared across the industry. Bargaining power and price sensitivity depend on relative firm sizes, product differentiation, available alternatives, switching costs, contract size, and relative importance of the deal to each firm. Vertical integration eliminates the need to share profits but limits strategic flexibility and adds operational complexity.

· Potential competition from new entrants or substitutes depends on barriers to entry. Incumbents erect barriers to entry to deter potential competition and safeguard future profits. Possible moats include product differentiation, economies of scale, capital intensity, distribution capacity, brand loyalty, regulatory requirements and switching costs.

Regulation, complements and technological change are three other forces relevant in some, but not all, markets. Regulation may alter industry structure such as when licensing and import taxes limit competition or subsidies lower prices for some consumers. Complementary markets may also influence demand and industry structure; for example, adequate charging infrastructure is a precondition for widespread adoption of electric vehicles. I will discuss technology change in the next section.

Industry structure is discernible at the outset and becomes clearer as industries mature. Industries with undifferentiated products and low capital requirements will have many firms who are price takers. Innovators and investors consider these uninteresting markets, though economists quizzically call this “perfect competition”. Industries with differentiated products, network effects or economies of scale will have few companies with pricing power.

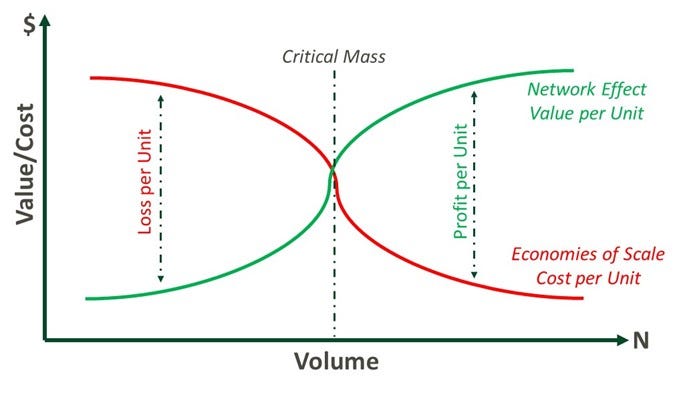

Most industries experience diminishing marginal returns but those with network effects and economies of scale enjoy increasing returns to scale. As Figure 3 illustrates, firms with high fixed or startup costs enjoy economies of scale where unit costs decline as volume increases. Firms enjoy network effects when value to customers increases as volume expands as is the case for social networks, the Internet or telephony.

Industries with high network effects or economies of scale are Winner Take Most markets. Most of the world’s largest and most valuable companies are in Winner Take Most Markets. These markets offer increasing returns to scale as unit economics are negative (firms lose money on each additional unit sold) when volumes are low but become highly profitable after firms reach critical mass.

Figure 3: Winner Take Most Markets — Increasing Returns

Venture investors target Winner Take Most Markets as initial capital requirements are sizable while potential returns are high for winning firms. Because few firms survive in Winner Take Most Markets, venture returns are subject to the Power Law where 80–90% of returns typically come from 10–20% of investments.

After introducing the Five Forces Model in Competitive Strategy in 1980, Porter described three predominant strategies firms pursue in Competitive Advantage in 1985: (1) cost leadership; (2) differentiation; and (3) focus on niche markets. As illustrated in Figure 4, companies risk getting “stuck in the middle” if they are neither cost leaders nor offer a differentiated product for which customers are willing to pay a premium.

Figure 4: Competitive Advantage — Potential Strategies

Making History: The Entrepreneur, Markets and Timing Revisited

Entrepreneurs have more influence on markets than Porter and the Five Forces Model suggest. Technology shifts may create windows of opportunity for startups to compete with incumbents, especially when new technology alters industry structure. Entrepreneurs who pursue disruptive innovation with new business models or technologies seek to reengineer industry structure to their advantage. I discussed this in detail in Social Capital: Six Strategies to Upend Incumbents.

Entrepreneurs may rearchitect industries by redefining industry boundaries. Existing customers served by incumbents define the Served Available Market (SAM), which is a subset of the Total Available Market (TAM). Entrepreneurs expand existing markets by targeting a niche market overlooked by incumbents or bridging market gaps to extend customer reach beyond those served by incumbents. A detailed discussion with examples of market extensions by bridging gaps is in Social Capital: Six Strategies to Upend Incumbents.

Entrepreneurs typically pursue Focused Differentiation using a Beachhead Strategy to target an underserved Market Segment. Beachhead Strategy derives from D-Day when nearly 7000 Allied vessels landed on just five Normandy beaches in France to overwhelm heavily fortified German defenses during World War II. Startups may similarly concentrate limited resources on niche, underserved markets to gain entry then extend to adjacent markets once the product is proven.

Bundling products by adding complementary products to enhance the overall offering may also shift competitive dynamics and alter industry structure. As noted earlier, the Five Forces Model ignores complementary products that are often vital to customer adoption. Xerox, for example, locks in consumers with subsidized prices for printers and copiers so they lock in customers and earn higher margins on recurring sale of ink cartridges. Microsoft, Apple and Google have extended their dominance in core markets by bundling offerings in adjacent markets. As artificial intelligence and online services lower entry barriers, entrepreneurs may find new opportunities to extend their footprint through bundling.

Finally, entrepreneurs may use timing, speed and adaptability to counter inherent incumbent advantages. As foretold in Competing Against Time: How Time-Based Competition is Reshaping Global Markets, speed often beats scale in rapidly changing markets. As the venture industry has grown, nimble startups now have access to capital to disrupt industries that were previously beyond the reach of innovative upstarts.

Does the person make the time or time make the person? In history, this is a false choice as the person makes the time only if timing is opportune. As we observe in the Three Cardinal Sins of Investing, the choice between markets and teams is also misleading as investors need to be in the right market with the right team. Entrepreneurs and investors should heed the sway of industry structure, which premeditates competitive dynamics and profitability. The Five Forces Model helps select markets wisely to allocate time, talent and treasure.

Yet entrepreneurs have more influence on industry structure than Porter and the Five Forces Model suggest. This article identifies five startup responses to the Five Forces Model and rearchitect industry structure more favorable to insurgents.

Do we invest in the markets or the team? We invest in both, but we invest in founders first.

Five Forces Model: Related Concepts

The Five Forces Model helps entrepreneurs and investors assess market attractiveness as competitive dynamics evolve across an Industry Life Cycle. Capital Intensive industries with high Barriers to Entry and Product Differentiation will have higher Market Concentration at maturity. Investors prefer Winner Take Most Markets, which enjoy Economies of Scale and/or Network Effects and offer Increasing Returns to Scale once firms reach Critical Mass. At Critical Mass, firms reach a Tipping Point or Inflection Point where growth accelerates. Firms with high Operating Leverage may become highly profitable once Unit Economics become positive.

Michael Porter promotes the First Forces Model to develop a strategy with a clear Value Proposition and Business Model in the pursuit of Competitive Advantage. Differentiation Focus with a Beachhead Strategy in a targeted Market Segment is typically best for venture backed startups. A SWOT Analysis identifies competitive strengths and weaknesses. The BCG Growth Share Matrix highlights the importance of Market Share within a Market Segment for profitability and strategic optionality as an industry matures.